It's been almost 45 years since Jack Bogle founded the Vanguard Group and launched the very first index fund. The launch of the Vanguard 500 Index Fund (VFINX +0.00%) got off to a rather inauspicious start, only raising $11 million -- less than 8% of the $150 million goal -- and leading many in the investing community to call it "Bogle's Folly."

But over the past decade, index investing has become the default wealth-building tool for millions of Americans. And none other than Warren Buffett credits Bogle as having done more than anyone else for the American investor.

There's little to argue with in that statement. Index funds have driven down the costs of investing, as well as improving returns, for the average person. But with hundreds of index funds out there to choose from, even index investing can be confusing. Furthermore, picking a fund that doesn't align with your short- and long-term goals could harm your returns, or even cause you to lose money.

So which index funds are the best choices? What exactly is an index fund? We'll answer those questions below, and share the top index funds for 2019 and beyond.

The proper allocation in these index funds can help you maximize your rewards, while minimizing your risk. Image source: Getty Images.

What is an index?

An index is a collection of stocks, bonds, or other asset classes based on certain criteria and weighting. For instance, the S&P 500 is an index of around 500 of the largest U.S. public companies. The companies included can (and do) change from year to year, as companies merge, go private, get acquired, or simply find themselves surpassed by smaller companies that have gotten bigger.

There are indexes for just about every industry; indexes tracking small-cap, high-growth stocks; indexes tracking stocks that pay high dividends, or have records of dividend payout growth; indexes of stocks in certain international markets. The list goes on and on.

And that's just stocks; there are also indexes for bonds, commodities, and even currencies. For the sake of clarity, this article will focus on the two primary kinds of assets available in index funds that most retail investors should own: stocks and bonds.

What is an index fund?

An index fund is a financial instrument you can buy to own a stake in all of the components of a specific index. Each index fund tracks a specific index of stocks, bonds, or other financial assets.

If you invest in a S&P 500 index fund, you'd actually own a small piece of each of the 500 components of the S&P 500, and your returns would very closely match that index. That's how it works for every other index fund, too. If you chose to invest in the Energy Select Sector SPDR you would own a piece of the 29 energy industry stocks in the S&P 500, which is what the Energy Select Index tracks.

The fund manager who runs the fund allocates the investments in the fund to match the construction of the index the fund tracks, collecting a fee -- called the expense ratio and expressed as a percentage of the assets held -- to cover expenses (and make some profit) to run the fund.

Pros and cons of index funds

Why choose an index fund, instead of a fund run by a manager who actively chooses the stocks or other assets in which the fund invests? In short, because the vast majority of actively managed funds underperform the index they benchmark their performance to, while charging expenses that can easily be double or triple what you'd pay for an index fund. The evidence is undeniable: Passively managed index funds outperform actively managed funds to an overwhelming degree, both from one year to the next, and over the long term.

Simply put, index funds are more likely to make you more money.

Furthermore, index funds also provide a great way to diversify, whether it's across a broad selection of stocks like the S&P 500, within an industry, or across a category of stocks. As compared to picking just a few individual stocks, this diversification can significantly reduce your risk of permanent losses from a single company going under.

At the same time, index investing has drawbacks. Chief among them is that by indexing, you're settling for average returns. Sure, outperforming the stock market isn't easy, but it's not impossible. Eschewing individual stocks for index funds can reduce some downside risk, but also caps your potential returns to the combined results of a big basket of companies.

Fortunately, there's no law requiring you to choose only one path or the other; plenty of successful investors use a combination of index funds and individual stocks to fit their personal risk-reward profiles.

What are the different kinds of index funds?

While there are hundreds of different index funds in which you can invest, they generally fall into one of the following groups:

- Stock index funds

- Bond index funds

- Real estate index funds

- Target-date index funds

Stock index funds

These funds generally fall into broad categories based on broad stock-market indexes, such as the S&P 500, Dow Jones Industrial Average, or Russell 2000, or narrower categories focusing on specific industries or even subsectors of an industry. Stock index funds can also focus on specific geographical regions, such as emerging markets, or more broadly represent the entire global economy.

The key thing to understand about any stock index is that this category of index funds will be the most volatile. In general, stock funds are described as being the most "risky," but that risk is generally more concentrated in short-term movements. The recent stock-market sell-off provides an excellent example of this short-term volatility risk:

VFINX Total Return Price data by YCharts.

From Oct. 3 to Dec. 24, 2018, stocks lost essentially 20% of their value. Needless to say, taking a 20% loss on your investments in less than three months is scary and painful. However, as the chart above also shows, stocks recovered from those losses within a few months.

The example above is not unusual. Historically speaking, the market has averaged a 10% drop once a year, and a 20% (or more) drop once every five years or so. These drops are unpredictable and happen very quickly. This is why stock investments -- including every index fund that holds stocks -- are not where you should risk money you plan to spend in the short term.

However, stocks generally bounce back very quickly from these sudden and unpredictable sell-offs, and then continue to deliver positive gains, making them an ideal asset for building long-term wealth. The key is not selling in a panic at the first sight of a drop, instead maintaining a long-term focus and holding accordingly when everyone else is selling on short-term fears.

Bond index funds

Like stock index funds, these offer a simple, low-cost way for individual investors to own a diversified portfolio of bonds and similar fixed-income assets. Unlike stocks, bonds are generally far less volatile in the short term. This is because the value of a bond is relatively easy to determine: the dollar value of the bond itself when it matures, plus the interest that the company or government issuing the bond agreed to pay.

The result is that, in general, a bond price will only fluctuate based on changes in interest rates. If rates went up, the value of a bond -- if you were to sell it before maturity -- would go down, since a new bond issue today would pay higher interest. Conversely, if interest rates fell, the value of your bond on the secondary market would rise, since it would yield higher interest than new issues. And since interest rates don't fluctuate significantly from one day to the next, bond prices are typically very stable.

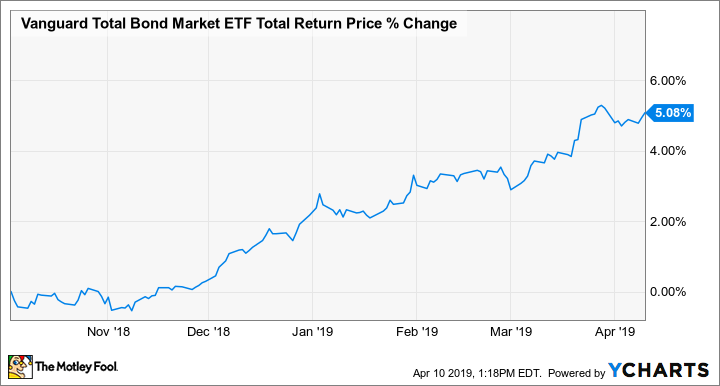

Yes, economic and geopolitical uncertainty can cause bond prices to fluctuate a little more than changes in interest rates, but that's still far less than stocks. Here's a look at the Vanguard Total Bond Market ETF, which tracks the Bloomberg Barclays U.S. Aggregate Float Adjusted Index, over the same October-to-April period as the chart above:

BND Total Return Price data by YCharts.

As you can see, this bond fund, which owns a "wide spectrum of public, investment-grade government and corporate bonds, as well as investment-grade mortgage-backed securities," lost less than 1% of its value even as stocks fell sharply; over this very short period it rewarded investors with 5% in total returns (which includes the interest paid) while many stocks were still down in value.

This is why bonds -- and for most of us retail investors, this means bond funds -- can be ideal investments for shorter periods of time: You can't afford the risk of your assets falling in value by 20% (or even more) right when you might need to sell them for cash.

Real estate index funds

These funds invest in stocks, primarily in a specific category of companies called real estate investment trusts, or REITs.

REITs are companies that own office buildings, hotels, data centers, industrial facilities, apartments, shopping centers, and just about any other type of real estate you can think of. Real estate values are generally quite stable, and the cash flow REITs earn from their real estate holdings also tends to be far more stable than the earnings of other types of businesses during economic weakness. For these reasons -- and the fact that REITs are required to pay out 90% or more of their net income in dividends, making them popular income investments -- real estate investments are generally less risky as a class than other kinds of stocks, if still higher-risk than bonds.

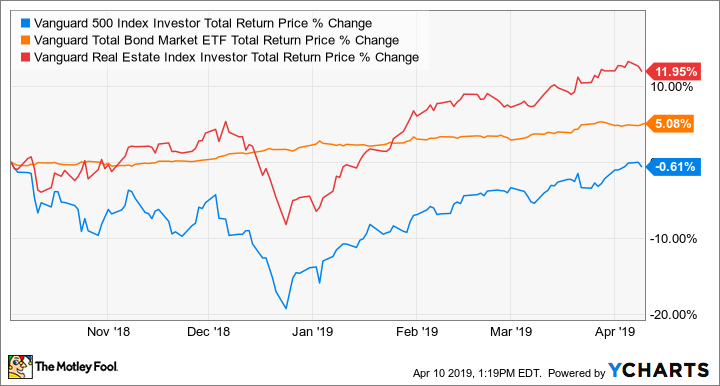

As an example, let's take the same time period we used above, and add the Vanguard Real Estate ETF to the mix:

VFINX Total Return Price data by YCharts.

As the chart shows, REITs still lost value during this quick stock-market sell-off, but fell far less than other stock classes. They also rebounded sharply and very quickly, but they did lose value, and far more than bonds. The lesson here is that real estate investment trusts may be lower-risk in the short term than other classes of stocks. But they're still stocks, and that means short-term volatility far greater than bonds.

Target-date funds

Target-date funds aim to provide investors with a simple, single-investment tool to own the proper mix of stocks and bonds, based on an expected retirement date.

For example, if you plan to retire about 20 years from now, the Vanguard Target Retirement 2040 Fund (VFORX +0.00%) might be a reasonable choice. This fund holds about 85% of its assets in two broad stock-market index funds (one domestic and one international), and the remaining 15% in two broad bond-market index funds (one domestic and one international). It charges investors only the underlying expense ratio (currently 0.14%) of those four funds.

Over time, the fund manager will gradually adjust the mix of the portfolio to a higher percentage of bonds. For comparison, the Vanguard Target Retirement 2030 Fund (VTHRX +0.00%), for people looking to retire in about 10 years, is composed of 75% stocks and 25% bonds; this reduces the impact of market downturns, since it holds fewer stocks.

However, these target-date funds are all held as a single investment, so when you do sell assets for cash, you're selling stocks and bonds. This makes them less-than-ideal holdings when you're actually in retirement, and may be actively selling off assets for cash.

Index mutual funds vs. index ETFs

At their core, shares of an index mutual fund and an index ETF (exchange-traded fund) are essentially the same thing: A stake in a broad collection of the stocks or bonds that make up a particular index. They differ in how and where investors can buy and sell them:

- A mutual fund doesn't trade on a stock market; it's generally purchased directly from the fund manager, or through partner brokers.

- An exchange-traded fund can be bought and sold on a stock exchange.

Since ETFs trade on stock exchanges, they are highly liquid, and you can buy and sell them (generally within moments) during regular market trading. Mutual funds are far less liquid, since buying and selling doesn't take place on a market between investors, but directly with the fund.

Furthermore, the fees investors pay when buying or selling a mutual fund are different than with an ETF. With an index mutual fund, you typically pay no trading fees or commissions up front; however, you may be required to hold your investment for a minimum amount of time, often a few months, before you can sell without paying a fee. With an index ETF, since you're buying and selling on a stock exchange, you can trade as often as you like, but you'll have to pay whatever commissions or fees your broker charges for each trade.

How do you know which index funds are right for you?

This is where personal financial advice can come in handy, particularly from someone who is held to the fiduciary standard (meaning they're obligated to act in your best interest) versus a suitability standard (meaning they can act in their best interest over your own when making recommendations). A reputable advisor, such as a Certified Financial Planner, can help you identify your short- and long-term financial goals, so you can then choose appropriate investments to reach those goals.

For instance, the Vanguard 500 fund is an excellent investment, and frankly one that nearly every kind of investor at every life stage should own shares of. But for people who are already retired and counting on their investments for income today, having all of their assets in stocks could cause substantial financial harm if they're forced to sell assets for income in the middle of a market crash. Retirees would have been better off holding cash and bonds for immediate and shorter-term needs, so they wouldn't have to tap their stock holdings in a stock-market downturn.

On the other side of the same coin, young investors wouldn't want to make the opposite mistake to avoid short-term losses, and have too much of their nest eggs invested in bonds. This is because bonds -- both historically and at current interest rates -- simply can't match stocks for long-term returns. Young investors who avoid stocks would arrive at retirement with a much smaller amount of wealth than if they had owned more stocks.

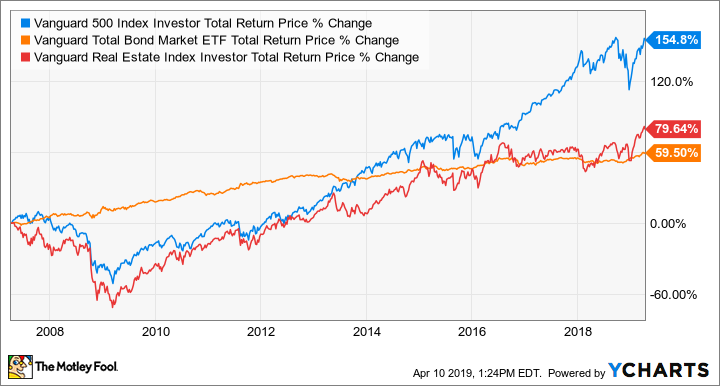

While we've seen how short-term volatility can affect different kinds of index funds, we haven't shown how the returns play out over the long term:

This chart shows how three broad-based index funds, in U.S. stocks, bonds, and real estate, performed from early 2007 to early 2019. This period of time is particularly important: It starts near the stock market's peak, prior to the global financial crisis which caused the Great Recession of 2008-2009, when stocks would lose nearly 60% of their value at the bottom.

As you can see, stocks got absolutely smashed in 2008 and 2009, and real estate stocks -- remember that real estate financing was at the heart of the crash -- took an even worse beating. Bonds, however, held up incredibly well, even during one of the worst economic periods since the Great Depression. That's bonds for the win if you have short-term needs, such as retiring, purchasing a home, or paying for a child's college education in the next three to five years.

However, once you get past that five-year mark, the long-term earnings growth of stocks starts to really show off, with the Vanguard 500 delivering almost triple the returns of bonds over the 11 years we're studying. Even real estate stocks, coming out of the worst real estate crisis in modern history, delivered significantly better long-term returns than bonds -- $2,000 more in returns on a $10,000 investment.

The key lesson here is that, when it comes to picking the right mix of index funds in your portfolio, you shouldn't think as much in terms of risk -- particularly if that's defined as volatility -- as in terms of time line. For instance, if you're still 20 years from retirement, your portfolio can -- and should -- take on far more volatility than someone who's two years from retirement; you can ignore the ups and downs and continue to hold, for far better long-term returns.

Let's take a closer look at five top funds that have a place in just about every investor's portfolio. (In four cases, you have the option of a mutual fund or an ETF; the fifth is an ETF.)

The top five index funds for 2019

| Index Fund (Mutual Fund or ETF) | Expense Ratio | Description |

|---|---|---|

| Vanguard 500 Index Fund Admiral Shares (VFIAX +0.88%) & Vanguard S&P 500 ETF (VOO +0.84%) | 0.04% | Large-cap U.S. stock index fund; tracks the S&P 500 index of U.S. stocks |

| Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX 0.20%) & Vanguard Total Bond Market ETF (BND 0.15%) | 0.05% | Bond index fund, comprising government and investment-grade corporate bonds; tracks the Bloomberg Barclays U.S. Aggregate Float Adjusted Bond Index |

| Vanguard Real Estate Index Fund Admiral Shares (VGSLX +0.00%) & Vanguard Real Estate ETF (VNQ 0.38%) | 0.12% | Real estate stock index fund; tracks the performance of the MSCI US IMI Real Estate 25/50 Index |

| Vanguard Health Care Index Fund Admiral Shares (VHCIX +0.00%) & Vanguard Health Care ETF (VHT +0.83%) | 0.10% | Healthcare stock index fund; tracks the performance of the MSCI US IMI Health Care 25/50 Index |

| Schwab Emerging Markets Equity ETF (SCHE +0.93%) | 0.13% | International stock index fund, comprising non-U.S. large- and mid-cap stocks in emerging markets in Asia, South America, and Africa; tracks the FTSE Emerging Markets Index |

The top large-cap stock index fund

The Vanguard 500 Index Fund remains one of the best index funds for the majority of people to own in order to achieve their long-term financial goals. As discussed above, this fund tracks the S&P 500, which makes up some 80% of the market value of the entire U.S. stock market, and has proven to be a solid long-term wealth builder.

One of the key things that makes this fund so appealing is that it's very inexpensive to invest in, charging an ultra-low 0.04% (that's $4 for every $10,000 invested) expense ratio. There are two different ways to invest in this fund, as it's available in both a mutual fund and an ETF. Depending on a few factors, one may be a better choice than the other.

Vanguard 500 Index Fund Admiral Shares is the mutual fund, while the Vanguard S&P 500 ETF is the ETF. The mutual fund requires a minimum initial investment of $3,000, so if you're just getting started investing, buying into the ETF with the lowest-cost brokerage you can find is the best way to go.

Why this fund now? In short, the U.S. stock market has an incredible track record of delivering great returns. Over the past 50 years, the S&P 500 has averaged more than 10% in annualized returns, and with the growth of the global economy underpinning substantial opportunity for most U.S. stocks, the future continues to be very bright.

Furthermore, the S&P 500 fund looks reasonably priced, trading at a lower earnings multiple than it has for much of the past three years or more.

Add it all up, and you have a solid combination of value: low costs, with a minuscule expense ratio; market ETF and mutual-fund options for your particular needs; and -- most importantly -- the incredible opportunity for years of growth, in both developed and emerging markets.

The top bond index fund

Another offering from Vanguard, the Vanguard Total Bond Market Index Fund Admiral Shares and the corresponding Vanguard Total Bond Market ETF, makes the cut as the top bond fund for the vast majority of individual investors.

This fund has 70% in U.S. government bonds across short-, intermediate- and long-term maturities, with the remaining 30% invested in high-quality investment-grade corporate bonds. Its expense ratio of 0.05% (or $5 per year for every $10,000 invested) makes it one of the lowest-cost bond funds available. The Admiral Shares version has a $3,000 minimum initial investment, and the ETF is subject to brokerage fees and commissions, but this fund is an excellent way to gain exposure to a high-quality swath of bonds without giving too much of your yield back to a fund manager.

At recent interest rates, this fund earns around 2.8% in yield. That's far below the yield that bond investors have historically enjoyed:

Unfortunately, that's the reality of the current interest-rate environment, though recent rate increases have improved the yield from its low of around 2.4% a few years ago.

More importantly, this bond fund isn't designed to deliver the best yield; its purpose is to keep your investment dollars as safe as possible while delivering some yield.

Over the past decade, this index fund's worst full year was 2013, when it lost about 2% in total value after interest earned, in an extraordinarily volatile year for interest rates:

VBTLX Total Return Price data by YCharts.

Add it all up, and this fund has been a solid tool for capital preservation, while earning at least enough yield to offset the value-eroding impact of inflation. With rates set to remain low for years to come, this fund won't make you rich, but it will certainly help you keep what you have while earning you more interest than a savings account.

The top real estate index fund

Another Vanguard fund tops the list here: The Vanguard Real Estate Index Fund Admiral Shares and aforementioned Vanguard Real Estate ETF both track the MSCI US IMI Real Estate 25/50 Index, which includes around 190 high-quality companies and focuses on equity REITs.

The exact same characteristics of the two prior Vanguard funds apply here: The Admiral Shares mutual fund requires a $3,000 minimum initial investment, while the ETF trades on a stock exchange, and will be subject to your broker's fees and commissions.

This fund makes the top of the list for two reasons. First, the dividends paid by its REIT components and passed along to investors make it an excellent choice for investors looking for a dependable source of income, and an asset that's slightly more stable than more volatile classes of stock. Second, while the payout can fluctuate from quarter to quarter, since the component REITs pay dividends at different times, the long-term trajectory of the dividend should continue to grow.

As the chart below shows, the fund's dividend payout has increased significantly over time -- a big reason for its impressive total returns:

Furthermore, with an expense ratio of 0.12% -- or $1.20 per year for every $1,000 invested -- this fund is substantially lower-cost than most other real-estate funds available to retail investors.

If stocks continue to deliver the strong returns we've seen over the past decade, real estate isn't likely to outperform the S&P 500. However, if stocks don't keep rolling, or if there's a persistent period of lower-than-average returns, having a stake in a high-yield real estate index fund like this could go a long way toward helping balance your returns. So whether you're already retired or still many years away, this Vanguard fund should be on your list.

The top healthcare stock index fund

We've offered up a solid foundational investment in the Vanguard 500 index fund, and two important index funds to help balance your returns and limit losses with the bond and real estate index funds. But investors of nearly every stripe should also invest for growth. Even newly retired or soon-to-retire folks should be thinking about asset growth, since the average 60-something American will live to -- and potentially far beyond -- 80 years of age.

Speaking of extended life expectancies, not to mention two huge demographic shifts: If there's a segment of the global economy investors should make sure they have significant exposure to, it's healthcare. Americans are living longer than ever before, and the Baby Boomer generation is in the middle of its transition to retirement. This shift is on track to create by far the biggest population of seniors in history, with the population of people over 65 likely to break 80 million by 2029, while the over-80 population should reach 40 million around the same time.

For context, those numbers represent a doubling of the population of older Americans from 2010. Here's the real kicker: A 2017 Bank of America Merrill Lynch study estimates that the average couple who are 45 today will spend over $1.7 million on healthcare after they retire.

The Vanguard Health Care ETF, which tracks the MSCI US IMI Health Care 25/50 Index, gives investors direct exposure to over 380 of the top companies in biotechnology, healthcare equipment, managed health, pharmaceuticals, and healthcare services. This index fund is also available as a mutual fund, but with a minimum initial investment of $100,000, that's simply out of reach for many investors.

It's not just the transition of Baby Boomers into retirement that's set to drive healthcare spending higher. The global middle class is expanding rapidly, with The Brookings Institution estimating that it will increase by 1.7 billion people over the next decade. Members of this growing middle class won't just be buying iPhones and automobiles: They'll also use their new upward mobility to improve their quality of life through better healthcare.

Healthcare as a category is already starting to prove itself as a market-beating investment. Over the past decade, the Vanguard Health Care ETF has outperformed the S&P 500:

And this trend could accelerate in the future. If it does, making the Vanguard Health Care ETF a part of your portfolio could pay off incredibly well.

The top international stock index fund

Just as healthcare spending is set to rise on the back of a growing global middle class, plenty of winning companies are sure to be finding their way today outside of the U.S. For this reason, taking a small stake in the Schwab Emerging Markets Equity ETF could really pay off.

What makes this index fund unique among many other international index funds is that it excludes developed markets like Europe and the U.K., which are dominated by large multinational corporations. On one hand, exposure to some of Europe's biggest companies can be good, since it reduces the downside risk from too much exposure to emerging-market stocks. On the other, it waters down the upside potential of companies that concentrate on China, Taiwan, Brazil, India, and other upstart economies. Furthermore, with an expense ratio of only 0.13% -- $1.30 per year for every $1,000 invested -- it's a low-cost way to attain concentrated exposure to these future economic superpowers.

Make no bones about it: This is a swing for the fences. The rest of your portfolio should be where you make up any potential losses if this index fund doesn't deliver. And since inception, it has been trounced by the market:

But much of this weak performance is tied to the awful start it had. For the first five years and change after launch, the fund lost almost 23% of its value, while the S&P 500 was gaining 85%:

SCHE Total Return Price data by YCharts.

That's not surprising, considering that many emerging markets struggled to bounce back following the global financial crisis. But since getting its legs back under it, the fund has started to deliver the kind of returns that emerging economies should drive for decades to come:

SCHE Total Return Price data by YCharts.

As the saying goes: nothing risked, nothing gained. And yes, there's still plenty of risk in markets like China, Brazil, and India, but today's emerging markets will be economic powers in decades to come. This fund is an ideal way to obtain concentrated exposure to those emerging markets, so long as you keep your investment size within what you're willing to risk.

Build a strategy -- and your portfolio -- based on your short- and long-term goals

Too often, people are told to invest based on their risk profiles. While it's important to understand your personal comfort with volatility, the reality is, risk is more a product of how long you can hold an investment (like an index fund) than anything else. In other words, don't buy stocks with money you'll need to spend in the next few years, and don't expect to get rich buying bonds to "avoid risk."

You need a strategy based on your time line and your financial goals. Then you can determine how much exposure you should have to different assets -- to reach your goals, for both the short and long terms.