The Nasdaq-100 index is home to 100 of the largest technology companies listed on the Nasdaq stock exchange. It's coming off a barnstorming two-year run, returning 53.8% during 2023 and a further 24.8% in 2024, but it's currently approaching correction territory with a drop of 9% from its record high.

Market downturns can be unsettling, but they are a normal part of investing. In fact, history shows they produce the best buying opportunities, because U.S. stock indexes like the Nasdaq-100 have always climbed to new highs over the long term.

With that in mind, this might be a great time to buy CrowdStrike Holdings (CRWD -7.39%) stock, which is down 26% from its record high. The cybersecurity giant just delivered a record set of financial results for its fiscal 2025 (which ended Jan. 31), and management reiterated its goal to more than double revenue over the next six years.

Image source: Getty Images.

A leader in artificial intelligence-powered cybersecurity

CrowdStrike suffered one of the worst outages in the history of the cybersecurity industry last year. On July 19, it released a corrupted software update that crashed 8.5 million of its customers' computers worldwide, causing chaos for their businesses. Investors thought CrowdStrike would experience a customer exodus and a steep drop in revenue following the incident, but the company has defied the doubters.

As it turns out, it's indispensable for most of its customers. The cybersecurity industry has a history of fragmentation, meaning organizations would have to piece together products from different vendors to achieve adequate protection.

However, CrowdStrike's flagship Falcon platform is one of the only all-in-one solutions on the market, featuring 29 modules (products) protecting cloud networks, identities, endpoints, and more, so it's very inconvenient for customers to move away from it.

NASDAQ: CRWD

Key Data Points

Falcon uses a lightweight, cloud-based architecture, and it leans on artificial intelligence (AI) to automate everything from threat detection to incident response, which eases the burden on cybersecurity managers who are dealing with a growing number of threats. CrowdStrike's AI models are trained on more than 2 trillion security events each day, so they are constantly becoming more accurate.

At the end of fiscal 2025, a record 67% of Falcon customers were using five modules or more, which was up from 64% at the end of fiscal 2024. The Falcon Flex subscription option is driving some of that momentum, because it allows businesses to reallocate their spending to different modules when their needs change over time.

CrowdStrike says the average Flex customer has tried nine modules, so this subscription is a great way for the company to draw them into new products and entice them to spend more money.

CrowdStrike beat expectations in fiscal 2025

Shortly after the July 19 outage, management reduced its revenue forecast for fiscal 2025 by 2.5%, from $4 billion to $3.9 billion. It was a surprisingly small adjustment considering the magnitude of the incident, but CEO George Kurtz was confident because while many new deals were being delayed, he said the majority remained in the company's sales pipeline.

A few months later, in the fiscal 2025 third quarter, CrowdStrike even increased its annual revenue forecast to $3.93 billion (at the top of the range), which was yet another sign the outage was unlikely to leave any lingering effects on the business.

When the company reported its official fiscal 2025 results last week, its revenue beat the latest forecast and came in at $3.95 billion. It was a 29% increase from the prior year.

And it gets better: Management also reiterated its long-term goal to reach $10 billion in annual recurring revenue (ARR) by fiscal 2031. Since ARR ended fiscal 2025 at $4.2 billion, the forecast represents potential growth of 138% over the next six years.

The stock might be cheap when viewed through a long-term lens

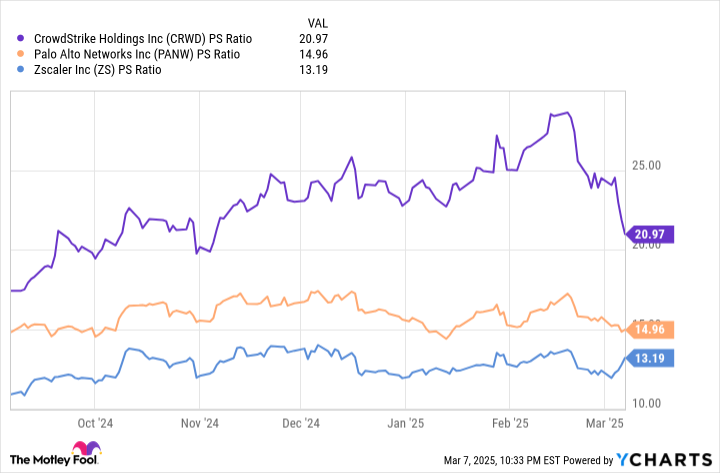

CrowdStrike stock trades at a price-to-sales (P/S) ratio of 20.9 as of this writing, which is a 29% discount to its long-term average of 29.5. However, the stock is still more expensive than some of its peers in the industry, including Palo Alto Networks and Zscaler:

CRWD PS Ratio data by YCharts.

With that said, CrowdStrike's revenue grew by 25% in its most recent quarter, outpacing Palo Alto's increase of 14%, and Zscaler's gain of 23%. As a result, it deserves a premium valuation. Plus, Palo Alto is CrowdStrike's biggest competitor, but it only just started transitioning to a platform cybersecurity approach, and a mere fraction of its customers are on board so far. That leaves CrowdStrike with a significant head start, which could also be a reason investors are paying up for its stock.

However, investors who buy into the CrowdStrike story today must be willing to hold for the long term. If we assume the company achieves $10 billion in ARR by 2031, that places its stock at a forward P/S ratio of just 8.2, meaning it would have to soar by 154% over the next six years just to maintain its current P/S ratio.

Here's the kicker: Management values its addressable market at $116 billion today and expects it to more than double to $250 billion over the next four years alone. Therefore, even if it achieves $10 billion in ARR, it will have captured only a fraction of the opportunity in cybersecurity.

Patient, long-term-oriented investors who are looking for a high-quality stock to buy in the midst of the recent market turbulence should definitely consider CrowdStrike Holdings.