Palantir (PLTR -4.71%) stock appeared to be in a bubble at the start of the year. Investors' expectations were incredibly high, and the valuation looked inflated. Following the hefty sell-off that hit most artificial intelligence (AI) stocks, however, Palantir is down 27% from its all-time high.

Some investors may see this decline as a sign the stock may be ready to roar again. However, investors should pay attention to this one metric, which hints that there could be more pain ahead.

Palantir's software is in huge demand

Palantir has become one of the hottest AI stocks on Wall Street. Its data analytics software has been around for a long time and was originally catered to government agencies. But in recent years, Palantir has expanded rapidly into the private sector.

While Palantir's base product is a strong selling point, the biggest hit lately has been its Artificial Intelligence Platform (AIP). AIP allows its users to do several things, but model integration and AI agents are the two most noteworthy. By integrating various AI models throughout an employee's workflow, Palantir's clients can control what sensitive information is fed into an AI model rather than having all of it shared with a third-party. Additionally, users can program AI agents to do tasks that humans normally would do, freeing them up to do work that requires more original thinking.

NASDAQ: PLTR

Key Data Points

AIP has been a huge growth driver for onboarding new commercial clients, but it also has been a way to expand government clients' spending.

This dual-market approach has fueled Palantir's massive growth as both sectors ramp up their AI spending. Palantir's government revenue rose 40% year over year to $455 million in Q4, while commercial revenue grew 31% to $372 million. But after six straight quarters of accelerating revenue growth, the question remains: Is it enough?

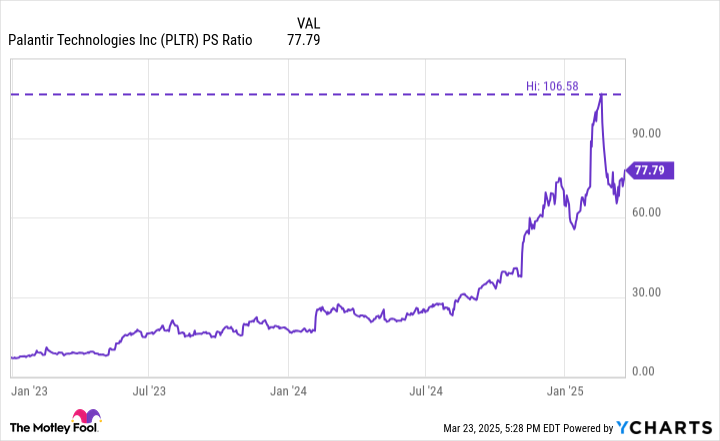

The stock is still in a bubble

Stocks enter a bubble when expectations outweigh reality. After Palantir logged a more than 1,800% gain in just over two years, this was absolutely the case as the stock traded for more than 100 times sales at its peak.

Data by YCharts.

Although the recent sell-off may appear to be an opportunity to buy the stock at a discount, shares are still far too expensive. To understand what kind of growth a 78 times P/S multiple conveys, let's model out the best-case scenario for Palantir based on these three assumptions:

- Revenue growth accelerates to 40% and stays at that level over the next five years.

- Profit margins nearly double from their current level of 16% to 30%.

- Any dilution from stock-based compensation is ignored.

That's a best-case scenario for the stock: The growth rate is higher than even what the company predicts. Management has guided for approximately 31% revenue growth this year, while Wall Street analysts believe Palantir will grow 32% in 2025 and 27% in 2026. Additionally, the 30% profit margin is a level that only the best software companies achieve, and Palantir's 16% margin isn't close to that level right now.

Regardless, if Palantir somehow achieves those figures, it will produce $15.4 billion of revenue and $4.6 billion in net income by 2029, a huge increase from the $2.9 billion and $462 million, respectively, reported for 2024.

However, based on the company's current market capitalization of $213 billion, those 2029 estimates still give the stock a price-to-sales (P/S) ratio of 13.8 and a price-to-earnings (P/E) ratio of 46.2. Both figures still represent a significant premium to the broad market, and they're based on absolute best-case scenarios for revenue growth and profit margins. Meanwhile the share count and stock price would have to remain unchanged.

In all reality, well over five years of bullish growth are baked into Palantir's stock price right now, which is far too much of a premium to pay. Investors should avoid the stock while it's still in its current bubble. There are better stocks to be buying in this marketwide sell-off.