Enterprise Products Partners (EPD 1.17%) has a lot going for it as an income investment. But there is one factor that might cause some investors to pause, and with good reason. Whether Enterprise Partners is a buy now really depends on what you are trying to achieve as an investors. Let's dive in and see.

What does Enterprise Products Partners do?

Enterprise Products Partners is a large North American midstream business. It owns energy pipelines, storage, processing, and transportation assets. It mostly charges fees for the use of its assets, which means that demand for energy is more important than the price of the commodities moving through its midstream system. Energy is vital to modern society, so demand for energy tends to remain strong, no matter what is going on in the world.

Image source: Getty Images.

Essentially, Enterprise operates in the most reliable and predictable segment of the broader energy sector. Its assets produce reliable cash flows through the energy cycle, and that, in turn, supports Enterprise's ability to pass cash on to unit holders.

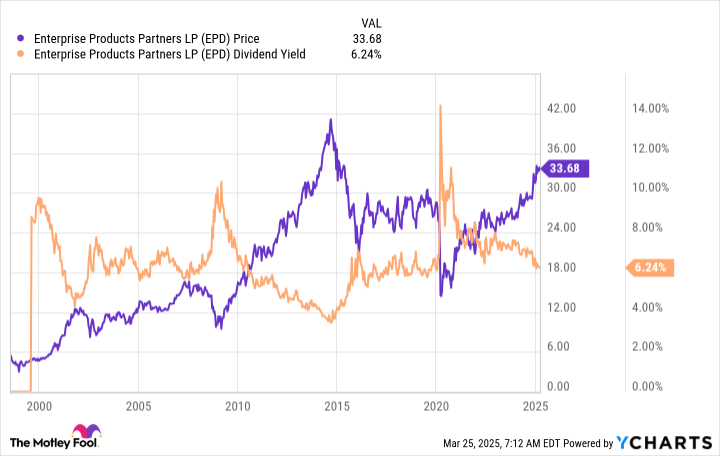

And it passes a lot of cash on to unit holders, noting the master limited partnership's (MLP's) lofty 6.3% distribution yield. That distribution has been increased annually for 26 consecutive years.

Enterprise Products Partners' balance sheet is investment grade-rated, and its distributable cash flow covered its distribution by 1.7x in 2024. These facts suggest there is a lot of leeway for adversity before a distribution cut would be in order.

So far, so good -- but do these facts make Enterprise a buy? It depends.

NYSE: EPD

Key Data Points

An attractive yield, but a less attractive price

If you are a dividend investor trying to live off of the income your portfolio generates, Enterprise's lofty 6.3% yield will be very attractive compared to other options. For example, the S&P 500 is only offering a 1.2% yield today. The average energy stock has a 3.1% yield. Given that landscape, if you are looking for a high yield from an energy stock, Enterprise will stand out.

But there's a caveat here. Enterprise's units have risen dramatically in price over the past five years. Given the 140% gain over that span, it is pretty clear that Enterprise is not nearly as attractively priced as it was not too long ago. Five years ago, the distribution yield was up around 13%. It was a much more attractive income investment back then.

However, what was happening back then is also important to remember. The low price and high yield were related to the uncertainty following the outbreak of a global pandemic. It would have been hard for many investors to have pulled the trigger to buy Enterprise at that point and, perhaps, it isn't a fair comparison of what to expect, given the unusual nature of the health scare at the time.

If you look further back at the yield trends for Enterprise, you'll see that 6% or so is about middle of the road for the midstream giant. Or, to put it another way, it looks like this high-yielder is reasonably priced. Deep value investors might not want to buy it, but if you are an income investor, the huge price advance over the past five years probably isn't a good reason to pass on Enterprise Products Partners.

The positives probably outweigh the negatives

Every investment comes with trade-offs. That's true of Enterprise Products Partners, which was much more attractively priced five years ago than it is today. However, for income investors, the current yield seems reasonable historically speaking and attractive relative to other income options. This midstream giant is probably worth buying today if generating a reliable income stream is your goal.