Healthcare diagnostics equipment manufacturer, Idexx Laboratories (IDXX 1.11%), is the global leader in pet care.

But here's an interesting tidbit: The company's shares have risen 10,230% since 2000, as Idexx quickly grew to corner a 15% market share of the $45 billion pet diagnostics industry.

Despite this incredible run, Idexx's current share price is the same as it was in late 2020, despite revenue growing by 50% and free cash flow (FCF) per share rising 87% over the same period.

This divergence between a company's improving financial results and its languishing share price is often a powerful combination for investors -- and I believe that could be the case with Idexx. It looks more dominant than ever, yet trades at 41% below its all-time highs. Here's why now looks like the perfect time to add to this proven winner.

NASDAQ: IDXX

Key Data Points

Meet this little-known S&P 500 multibagger

While Idexx Labs has been a 100-bagger over the last 25 years, the average investor may not have even heard of this lesser-known component of the S&P 500.

The company offers an assortment of point-of-care diagnostic equipment and services used to keep our furry friends healthy. When a veterinarian runs a complete blood count on a pet, measures glucose or liver enzymes, screens for heartworms or Lyme disease, or tests for pancreatitis, Idexx Labs has the equipment necessary.

It has over 147,000 of its instruments installed at veterinary offices across the world -- a figure that grew by 9% over the last year.

What makes Idexx an intriguing stock, however, is the recurring revenue it generates from this massive installed base of diagnostic equipment. After running a test using Idexx's equipment, a vet can analyze it in-house using the VetLab Station and make a diagnosis. Each test uses consumable products like slides, test cartridges, or cleaning solutions, creating a steady stream of recurring revenue for the company.

Furthermore, Idexx Labs also offers reference laboratory diagnostics and consulting services -- another recurring revenue stream. For example, a veterinarian may run a chemistry test on a dog and analyze it in-house to provide immediate, shorter-term care to make the pet comfortable. Then the vet could send the results to the reference lab for deeper analysis and a more detailed diagnosis with a long-term solution.

These VetLab and reference lab solutions (along with Idexx's other smaller recurring revenue sources) combine to equal nearly 80% of the company's total revenue, creating a large base of repeating sales.

Buoyed by the "humanization of pets" megatrend -- and with cats' and dogs' life expectancies increasing by two years since 2010 -- demand for these services will likely remain high. With our furry friends living longer and geriatric pets requiring twice as much wellness spending as one-to three-year-old animals, Idexx's equipment will play an outsize role in keeping senior pets healthy.

One final bit of excitement for investors (and a win-win for pet owners, too): Idexx Labs is launching a cancer diagnostics solution in 2025, which it hopes will expand to more than 50% of canine cancer cases within the next three years. The potential here is exciting on an investment level. It also makes the company the type of feel-good story that's fun to buy and hold, which is why it's one of my daughter's core holdings.

Image source: Getty Images.

Stock buybacks at a once-in-a-decade valuation

Powered by its higher-margin recurring revenue, Idexx Labs is a genuine cash cow and has been growing its profitability steadily over the last decade:

IDXX Profit and Owners' Cash Profit Margins data by YCharts.

Anchored by this growing profitability and FCF generation, the company has a decade-long history of returning almost all of its free cash flow to shareholders through stock buybacks.

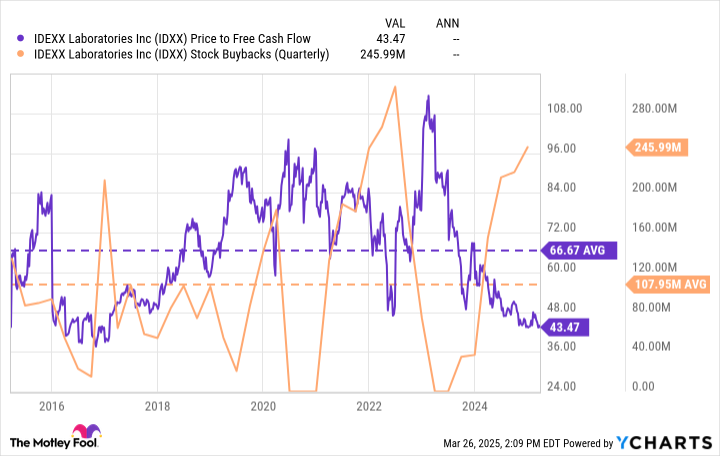

While management has historically done a great job of buying back shares when the company's share price dips, Idexx has averaged a price-to-FCF (P/FCF) ratio of 67 over the last decade:

IDXX Price to Free Cash Flow Ratio and Quarterly Stock Buyback Total data by YCharts.

This lofty valuation blunted the potential benefit of the stock buybacks for investors, yet Idexx still reduced its outstanding shares by 13% over that time.

However, with Idexx's valuation dropping down near once-in-a-decade lows, its recent ramp-up on buybacks could provide better shareholder value. With management planning to buy back roughly 4% of the company's shares in 2025 -- hopefully, while they remain at this lower valuation -- Idexx should receive a nice boost to its FCF-per-share figures over the coming years.

Although its P/FCF of 43 remains above the S&P 500's average of 33, I think Idexx's valuation is reasonable, thanks to its leadership position, stable recurring revenue, and resilient industry. With management buying Idexx's shares at a historically low valuation, I'm more than happy to buy alongside them and keep adding to this position in my daughter's portfolio.