A decade is a very long time on Wall Street, but I'm confident in my thinking that AGNC Investment's (AGNC -1.53%) shares will be worth less than those of Prologis (PLD -9.64%) and Rexford Industrial (REXR -8.89%) in 10 years. Here's why I believe investors who want a combination of income and capital appreciation will likely be better off with these two property-owning real estate investment trusts over mortgage-focused AGNC.

What does AGNC Investment do?

AGNC Investment is a mortgage REIT. It buys mortgages that have been pooled together into bond-like securities. It collects that difference between the yield on the securities it buys and its operating costs, which includes interest expenses since leverage is a key part of the business model. In some ways, AGNC Investment is more like a mutual fund than a company.

But the really important fact here is that AGNC Investment, despite offering a 14% dividend yield, is actually focused on generating a strong total return. In other words, to get the most out of this investment you would need to reinvest all of your dividends.

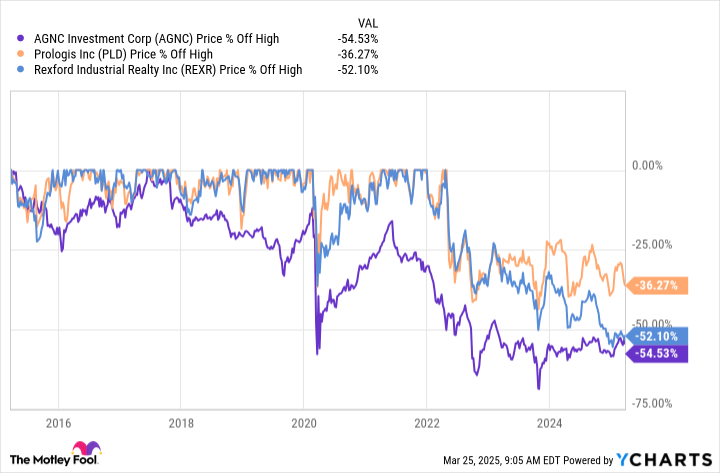

If you had done that over the past decade you would have made out reasonably well. If, instead, you used the dividends to pay for living expenses you would have been sorely disappointed with your outcome. As the chart above shows, you would have been left with less income and less capital.

What do Prologis and Rexford do?

Prologis and Rexford are property-owning REITs that focus on the industrial asset class. Prologis has a widely diversified portfolio with exposure to most of the world's major transportation hubs. Rexford is laser-focused on the Southern California market, which is one of the largest in the world but happens to be highly supply constrained.

These companies grow via the purchase, construction, and redevelopment of properties. In recent years they have also benefited from the rollover of expiring leases to new, higher rates. However, that trend appears to have peaked, leading investors to sell the stocks. From the peak in 2022, Prologis has lost around a third of its value while Rexford has lost about half of its value. That is, interestingly, roughly about what AGNC Investment's shares have lost over the past decade.

Why Rexford and Prologis will be worth more in a decade

There's an inherent difference in the business models here. Prologis and Rexford are purposely attempting to grow their businesses. So, in a decade, they should own many more properties than they do today. And, thus, their property portfolios will produce more rental revenue. Now that the industrial property fad investment theme has been cleaned up by big price corrections, investors are likely to begin rewarding Prologis and Rexford as they grow their businesses.

NYSE: PLD

Key Data Points

AGNC Investment, on the other hand, isn't exactly growing its business. It is simply trying to capture the difference between the yield on the securities it owns and its costs. That is a financial transaction and it doesn't really have as much to do with the growth of the business over time. Given the history, it is reasonable to expect that big dividends will be paid while the share price erodes further and the dividend gets cut. That is, after all, what has happened so far.

NYSE: REXR

Key Data Points

Even if the dividend were to increase leading the share price to rise, however, AGNC wouldn't provide the same kind of growth opportunity. That's because the operating businesses of Prologis and Rexford are fundamentally focused on growing. AGNC Investment's focus is on providing total return through the investment in bond-like securities. It is a very different approach, and one that won't interest most long-term dividend investors despite the mortgage REIT's lofty dividend yield.

Know what you own

Prologis and Rexford have tiny dividend yields relative to AGNC Investment, at 3.6% and 4.2%, respectively. But they both have a history of regularly increasing their dividends as the businesses backing those dividends grow. AGNC Investment, only looking to earn the spread between its costs and the interest it earns, has a history of dividend cuts behind it. At the very least, dividend volatility is likely to be the norm over time.

I would rather own a company focused on growth. That has a far higher chance of leading to a growing stock price compared to a REIT model that is more financial transaction than operating business. Which is why I expect both Prologis and Rexford to be worth more than AGNC Investment a decade from now.