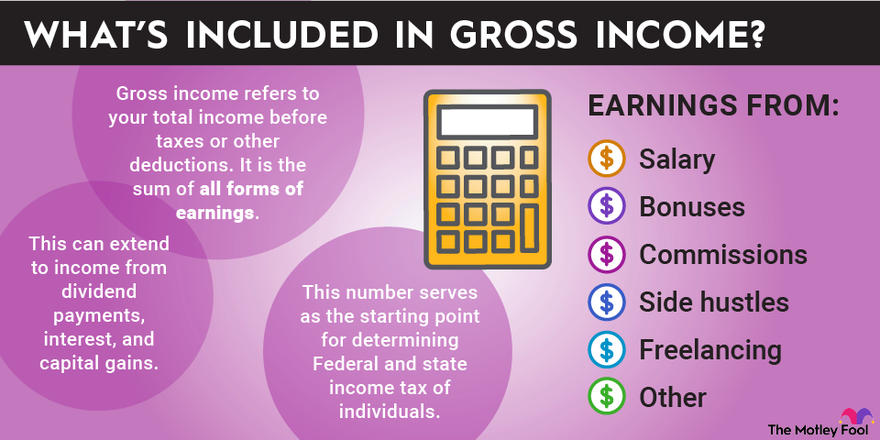

Gross income is your total compensation before taxes or other deductions. If you think of yourself as a business, your gross income is your top-line revenue.

This can be useful to know for a variety of reasons. For example, if you take out a loan, you'll have to pay monthly. Loan approval is usually contingent on your gross income exceeding a certain amount. Your gross income will also help in budgeting and in determining how much you'll have available to save for retirement.

It's also a much simpler measure than your net income, which requires you to account for taxes and other deductions.

Some of the common deductions, separate from taxes, include:

- Health insurance premiums

- Retirement contributions

- Commuter benefits

- Flexible spending account contributions

- Certain types of insurance (e.g., life, disability, supplemental)

Remember that gross income is your compensation before taxes and deductions, and your net income is the money you receive after taxes and deductions.

What to include in gross income

Gross income is the sum of all money earned during a particular period of time. This includes salary, bonus, commissions, side hustle, and freelance earnings, or any other sort of income, such as Social Security. Depending on the context, this can also extend to income from dividend payments, interest, and capital gains.

The one thing you won't need to do in calculating your gross income is account for taxes. Gross income is purely a pre-tax amount, so taxes won't be relevant to the calculation.

The importance of knowing your gross monthly income

If you're applying for a home or car loan, or if you're trying to develop a budget, it's important to know how much is coming in the door every month. Most lenders will need to know how much you earn to determine if you'll be a reliable borrower.

Knowing your gross monthly income can also help with deciding on an amount to save for retirement. If you're trying to determine how much to dedicate to your retirement account every month, knowing where you stand from a gross income perspective will help inform that decision.

Your net income is also of great importance. One way to think about net income is to see it as the "spendable" cash that actually flows through to your checking or savings account every month. Net income is also useful in developing a monthly budget since your regular after-tax expenses, both fixed and discretionary, will come from your net income.

Unfortunately, when you're quoted a salary of $75,000, you don't receive that amount in usable cash. A significant share of the money is dedicated to taxes and fixed deductions, so knowing your net income will help you develop a more stable budget and allow you to stay on top of your finances.

Calculating gross monthly income if you receive an annual salary

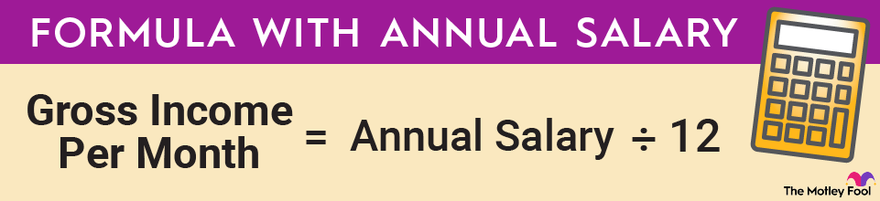

If you're paid an annual salary, the calculation is fairly easy. Again, gross income refers to the total amount you earn before taxes and other deductions, which is how an annual salary is typically expressed. Simply take the total amount of money (salary) you're paid for the year and divide it by 12.

For example, if you're paid an annual salary of $75,000 per year, the formula shows that your gross income per month is $6,250.

Many people are paid twice a month, so it's also useful to know your biweekly gross income. To find this amount, simply divide your gross income per month by 2.

Continuing with the above example, you'd divide $6,250 by 2 to arrive at $3,125 as your biweekly gross income.

Calculating gross monthly income if you're paid hourly

For hourly employees, the calculation is a little more complicated. First, to find your yearly pay, multiply your hourly wage by the number of hours you work each week and then multiply the total by 52. Now that you know your annual gross income, divide it by 12 to find the monthly amount.

(Note: If your hours vary from week to week, use your best estimate of the average number of hours you work.)

For example, if you're paid $15 per hour and work 40 hours per week, your weekly gross pay is $600. Multiplying this amount by 52 shows an annual gross income of $31,200. Finally, dividing by 12 reveals a gross income of $2,600 per month.

If you have any special circumstances, such as a certain amount of overtime hours per month or a recurring bonus or commission, you can generally add it to your gross monthly income.

The common way to do this is to determine the amount of overtime pay (or bonus or commission) you've received throughout the past year and divide it by 12. This amount would then be added to the gross monthly income you calculated from your base pay.

A note on adjusted gross income

You may have heard the term adjusted gross income or AGI, which is primarily used around tax time to describe your total income less certain deductions.

Without getting too heavy into tax language, AGI refers to a number found on your annual tax return and won't usually enter into the discussion of monthly gross income as it relates to your bimonthly paychecks.

Monthly gross income is simply the amount you earn every month before taxes and other deductions. Put another way, it's the annual amount you earn divided by 12. It's merely a basic measure to help with budgeting and other run-of-the-mill financial calculations.

Related investing topics

The bottom line

Knowing your gross monthly income is critical when it comes to formulating a budget and determining tax liabilities, retirement contributions, and other deductions. Gross monthly income also comes into play if you ever apply for a loan or submit paperwork to rent an apartment.

Finally, knowing the difference between gross monthly income and net monthly income is key. Your gross monthly income is all the money you actually earn, while your net income is the amount you can expect to actually hit your bank account every month. These amounts are very different, but they can easily get confused.

Having a handle on your monthly income is a great way to stay on top of your finances as a whole, so take the time to calculate it and know where every dollar is going.