You may want to perform a valuation calculation on your investments to ensure you're not overpaying. There are many different methods to this madness, but the Gordon Growth Model (GGM) is particularly well-suited for companies with steady dividend growth. Here's a closer look at this valuation technique.

What is the Gordon Growth Model?

The Gordon Growth Model helps investors calculate the intrinsic value of a stock based on future dividends that increase at a steady pace. It gets its name from Professor Myron Gordon of the University of Toronto, who originally published it in 1956.

The GGM is a popular valuation method and the most widely used of the dividend discount models (DDMs) for valuation. It assumes that a company's dividend grows at a steady rate in perpetuity, giving investors a present value of the company based on that future series of payments. The model works best on companies with stable dividend growth rates such as Dividend Aristocrats.

How to use the Gordon Growth Model

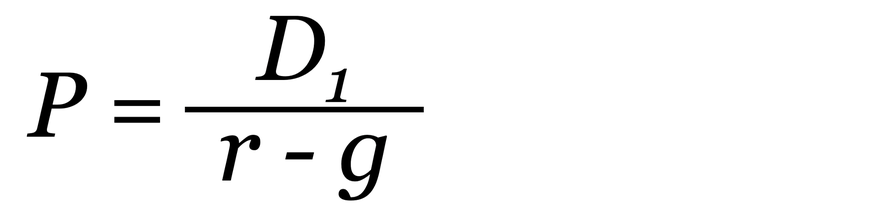

The Gordon Growth Model works best on companies that pay a steadily growing dividend and that an investor intends to hold for the long term. The three key inputs to the model are current dividend per share, average growth in dividend per share, and the required rate of return (i.e., the cost of equity capital). For calculating the valuation of a stock based off its dividends, the most commonly used formulation of the Gordon Growth Model looks like this:

Where:

- P = the stock's price based off its dividends (i.e., the theoretical valuation you are calculating).

- D1 = the stock's expected dividend over the next year. For this calculation, investors must assume that next year's dividend will grow at the company's historical rate of dividend increases.

- r = the required rate of return. This is the same as the company's cost of equity capital.

- g = the expected dividend growth rate. Investors can use either the company's historical average or its long-term dividend growth projection.

Or, to put it more simply, the Gordon Growth Model formula is this:

This formula calculates a stock's value today based on expected future dividends. Investors can then compare that value to the stock's current market price to see if it's worth buying.

Variations of the Gordon Growth Model

It's worth noting that there are several variations of the GGM. These include:

- The two-stage dividend discount model

- The three-stage dividend discount model

- The H-dividend discount model (H-DDM)

Each of these variations shares some similarities with the Gordon Growth Model. However, they don't assume a constant growth rate for the dividend. Instead, they account for a change in the dividend growth rate, which affects the present value discount factor and therefore the calculated present value of the stock.

For example, the two-stage model assumes the dividend grows at a steady rate during the first phase of its life before transitioning to a different rate for the remainder. Similarly, the three-stage model accounts for a third phase of dividend growth. Meanwhile, the H-DDM includes both initial and terminal growth rates for the dividend.

An example of the Gordon Growth Model

The Gordon Growth Model uses a relatively simple formula to calculate the net present value of a stock. For example, say a company expects to pay $2.50 per share in dividends over the next year, has a long track record of increasing its dividend 5% annually, and will likely continue to do so. It also has an 11% required return. Using this information, we can calculate the stock's value using the Gordon Growth Model:

$2.50 / (11% required return or 0.11 - 5% dividend growth rate or 0.05) = $41.67

Given that valuation, if the stock trades around that price, it's a fair value for investors. A price point well above that level suggests the market has overvalued the stock, while one considerably below it implies an undervalued stock.

Pros and cons of the Gordon Growth Model

There are several benefits to using the Gordon Growth Model, including:

- It helps investors put a firm value on a company's stock.

- It's easy to use.

- It's ideal for mature companies that pay steadily growing dividends.

- Investors can use it as an input for more complex dividend-based stock valuations such as the two- and three-stage models.

However, there are also several drawbacks. These include:

- It assumes that a company's dividend will grow at a constant rate in perpetuity. As previously noted, there are other versions that don't make this assumption.

- It's not suitable for companies that don't pay dividends or steadily increase their payouts. For example, the GGM generally has no use in valuing speculative, high-growth stocks.

- There are some potential issues with the relationship between the discount rate (cost of equity capital) and the dividend growth rate. If the required rate of return is less than the dividend growth rate, the model can yield a negative value. Conversely, if they're the same, it pegs a company's value at infinity.

A quick way to value dividend growth stalwarts

The Gordon Growth Model enables investors to quickly value a company that pays a steadily growing dividend. The goal is to provide a basis to determine whether the stock is trading at a fair valuation or not based on expected future dividend payments.

However, it's not a perfect model. Even the best companies don't always deliver bankable dividend growth. So, investors should use this model in conjunction with other methods of analysis in order to form a more informed opinion of a stock's intrinsic value. Even then, using it will still be more art than science, given that the only thing certain about the future is uncertainty.