However, this five-year rule differs in that it applies separately to each Roth conversion you make. Each new conversion starts its own five-year clock, and you'll need to account for multiple conversions to ensure you don't withdraw too much money too soon.

Note that the five-year rule applies equally to Roth conversions for both pretax and after-tax funds in a traditional IRA. That means if you're using the backdoor Roth IRA strategy every year, your "Roth contributions" are really conversions, and you can't withdraw them for five years without penalty.

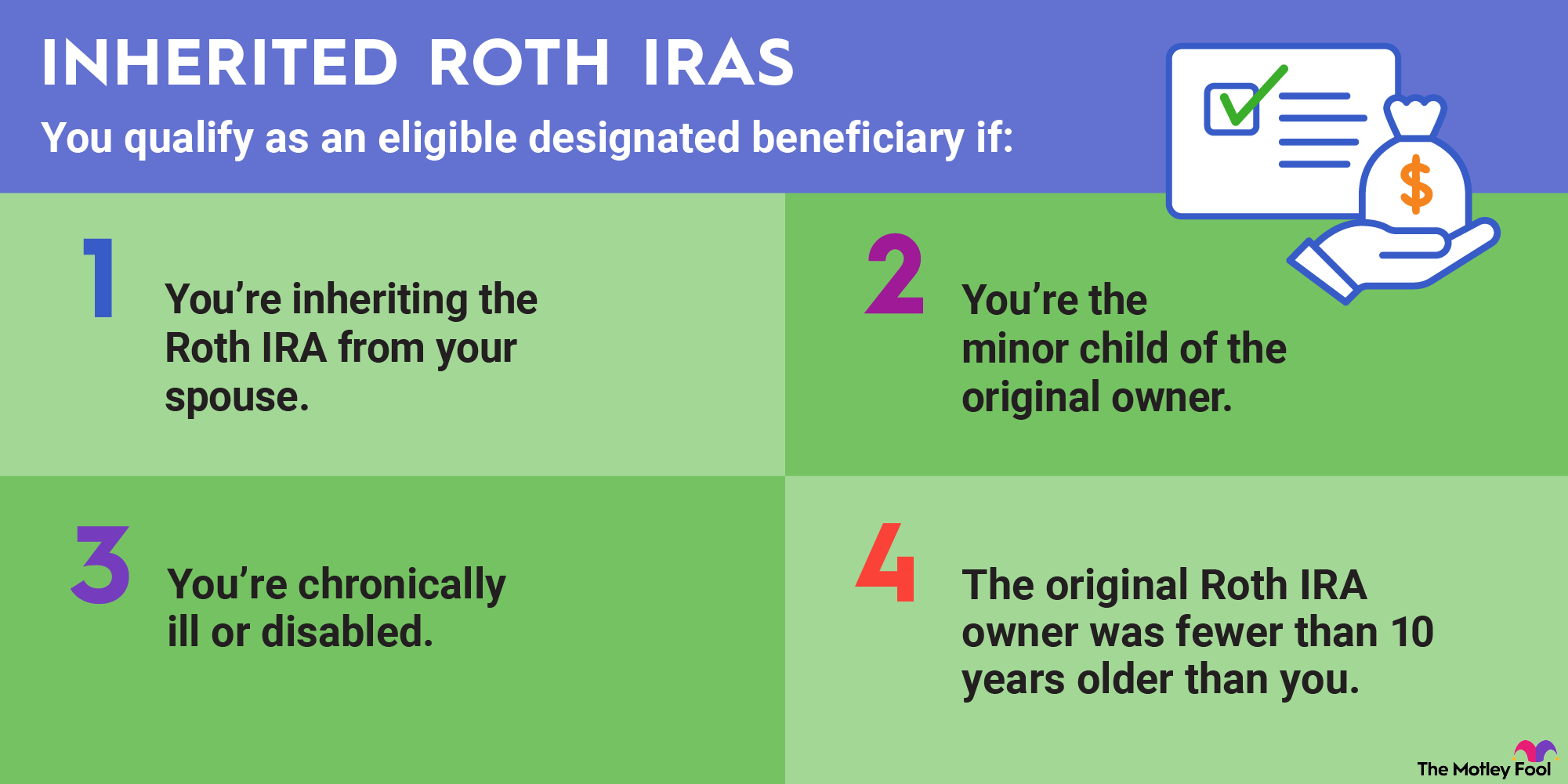

3. Inherited IRAs

If you inherit a Roth IRA from someone other than your spouse, you have a couple of options for withdrawing the funds. You have 10 years to deplete the inherited IRA, but RMDs may be necessary.

The 10-year rule applies only to Roth IRAs inherited from someone who died after 2019, per the SECURE Act rules. For Roth IRAs inherited from someone who died in 2019 or earlier, the pre-SECURE Act rules apply.

In the latter case, the 10-year rule is a five-year rule, meaning the account must be depleted by the end of the fifth year unless the beneficiary is taking annual distributions based on their life expectancy.

Inherited IRAs are also subject to the first-contribution five-year rule. Therefore, if it has been less than five years since the owner's initial contribution to a Roth IRA, the earnings are subject to taxation. Keep that in mind if you want to withdraw a lump sum early.