Nvidia (NVDA +1.36%) has been a dominant force in the AI computing market since the AI buildout began in 2023. However, viable alternatives are starting to pop up that could challenge Nvidia's dominance. If Nvidia's empire starts to crack, two stocks could soar in its place.

I think both are excellent buys for 2026 and are primed to soar, even if Nvidia can maintain its superiority.

Image source: Getty Images.

Taiwan Semiconductor

Nvidia designs graphics processing units (GPUs), but it doesn't manufacture them. Instead, it farms out that work to a handful of other companies. In the chip manufacturing world, that work primarily goes to Taiwan Semiconductor (TSM +2.74%). Taiwan Semiconductor is the world's largest chip foundry by revenue, and it has risen to that point thanks to continuous technological innovation and strong production yields.

NYSE: TSM

Key Data Points

Many of Nvidia's competitors also source their chips from Taiwan Semiconductor, so if Nvidia's dominance slips, Taiwan Semiconductor will be OK. Additionally, if Nvidia maintains its incredible grip on the artificial intelligence computing market, TSMC will continue to do great. All Taiwan Semiconductor needs to happen to succeed as an investment is for AI hyperscalers to keep spending like they are. If they do, Taiwan Semiconductor will be primed to soar in 2026, after all, it trades at a discount to the fabless chip companies.

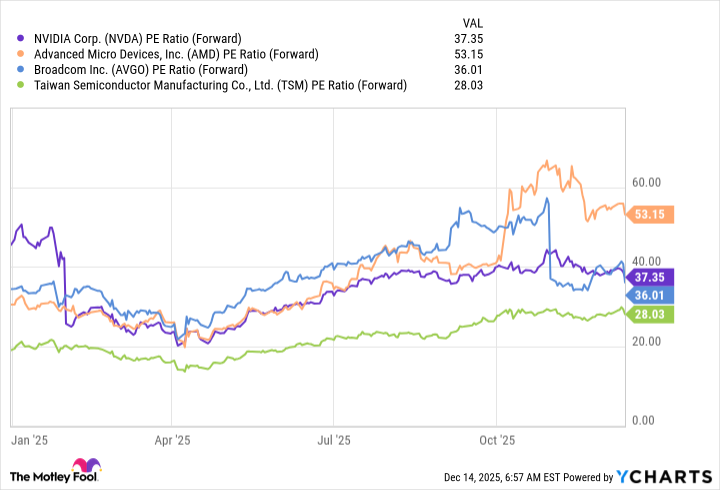

The three primary computing unit providers in the AI arms race are Nvidia, AMD (AMD +3.71%), and Broadcom (AVGO 4.48%). Nvidia is the largest of all of them, and happens to be the cheapest. But none of these three is cheaper than Taiwan Semiconductor.

NVDA PE Ratio (Forward) data by YCharts

Taiwan Semiconductor trades for 29 times forward earnings. That's a hefty discount to its peers, despite benefiting from the same tailwinds pushing these other stocks higher. I think this low starting valuation will play in its favor during 2026 and will be a key reason why it outperforms Nvidia in 2026.

Broadcom

Broadcom is taking a different approach than its peers to the AI computing problem. Instead of making a broad purpose GPU like AMD or Nvidia, it's partnering directly with the AI hyperscalers to build custom AI accelerators. These computing units aren't designed to handle a wide variety of workloads like a GPU is. Instead, it's designed specifically around the workload that it will see. By doing this, Broadcom can maximize performance while decreasing cost, only at the price of flexibility.

These computing units are surging in popularity, and Broadcom's financials reflect that. In Q4 (ending Nov. 2), its AI semiconductor revenue rose 74% year over year. For reference, Nvidia's data center division, which encompasses the GPUs primarily used for AI computing, increased revenue at a 66% pace. Broadcom is growing as a popular option to partner with, and I'd expect that trend to accelerate during 2026.

NASDAQ: AVGO

Key Data Points

However, Broadcom doesn't just make custom AI accelerator units. It has a whole host of other business units that make mainframe software and hardware, virtual desktops, cybersecurity, and countless other products. These divisions slow down Broadcom's overall growth rate, as evidenced by Broadcom's net revenue only rising 28% in Q4.

This could be what holds Broadcom's stock back from outperforming in 2026, but if the investment community is excited about Broadcom's AI prospects, it could soar past Nvidia. For Q1, Broadcom expects AI revenue to come in at $8.2 billion -- indicating a double over last year's total. This shows that Broadcom's AI growth rate is accelerating while others are moderating. Investors love to see accelerating growth, and if there is still appetite for AI investment, Broadcom's stock could soar past Nvidia's, especially if Nvidia starts to lose market share to more of Broadcom's custom AI accelerators.

I think both of these companies will do great in 2026, but I also wouldn't count Nvidia out, either. Owning all of these stocks may be a smart idea, as the AI buildout is far from over.